A recurring question is how to calculate changes in material costs. In principle, it’s quite simple!

Take Laspeyres’ formula and calculate how the material costs of a good have changed compared to the previous year.

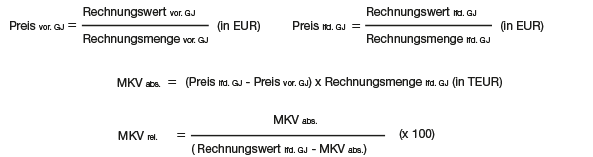

The prerequisite for calculating the “change in material costs (= MKV)” is recurring procurement processes based on numbered materials. This is done in order to be able to show the measurable contribution of purchasing to the company’s results. The main factors influencing this key figure are currency changes, predecessor and successor relationships, ancillary costs, discounts, material surcharges, and alloy surcharges.

But then it gets tricky:

The change in material costs can be viewed from different perspectives.

MKV with and without consideration of the supplier

The main variant refers to the consideration of the supplier. If a part is supplied by different suppliers, this can lead to different MKV values, depending on whether suppliers are grouped or not.

Example:

When the supplier is taken into account, the MKV is -134,849.

Without taking the supplier into account, i.e. at material level, the MKV is now -225,981.

This is because one of the suppliers had no volume in the previous year, so there is no change in material costs for this supplier. However, since this new supplier delivers the product at a significantly lower price, this results in an overall reduction in the costs for the product and thus a significant change in the MKV.

This clearly illustrates the effect of the change of supplier.